A champion NASCAR driver’s lawsuit against a giant insurer will provide financial advisors with front row tickets to a case testing one of the most complicated types of life policies.

Processing Content

Samantha and Kyle Busch accuse Pacific Life and an agent who sold them indexed universal life insurance policies of negligence, breaches of fiduciary duty and other violations of the law that cost them nearly $8.6 million in losses. The retirement income products were supposed to be “something safe and secure that would grow tax-free and protect our family long after racing” but instead “turned out to be a financial trap,” Kyle Busch said in

The suit has already revealed important takeaways for advisors and other practitioners, according to

“The IUL is powerful, but it is fragile,” Hood said. “A policy can either provide retirement protection or death benefit. There’s almost never enough money to do both, and they were, in essence, led to the plan by the retirement benefit aspect of it, but it was the death benefit that sucked all the money out of the policies and lapsed them within a seven-year period.”

READ MORE:

Case moved to federal court

Last month Pacific Life successfully petitioned to have the case moved from state court to federal court in Charlotte, North Carolina in a filing that cited the size of the Busches’ monetary claim and various geographic factors. (A lawyer for the Busches’ agent, Rodney A. Smith of Las Vegas-based Red River, did not respond to phone or email inquiries about the allegations.)

The company “does not comment on the specifics of individual matters” in order to “maintain the privacy and trust of our clients,” a Pacific Life spokesperson said in a statement.

However, Pacific Life’s business “has been built on providing valuable insurance products to help millions of families and businesses plan for their future financial security,” the statement said. “We stand by all our life insurance products, including indexed universal life (IUL). An IUL policy provides valuable life insurance protection, helping ensure that families and other beneficiaries receive financial protection in the event of an unexpected or premature death of a loved one. IUL also offers the opportunity to build cash value over time, which may be accessed for a variety of purposes, including supplementing retirement income. It is important that individuals work with their financial professionals to help ensure their intended insurance needs and financial objectives are met.”

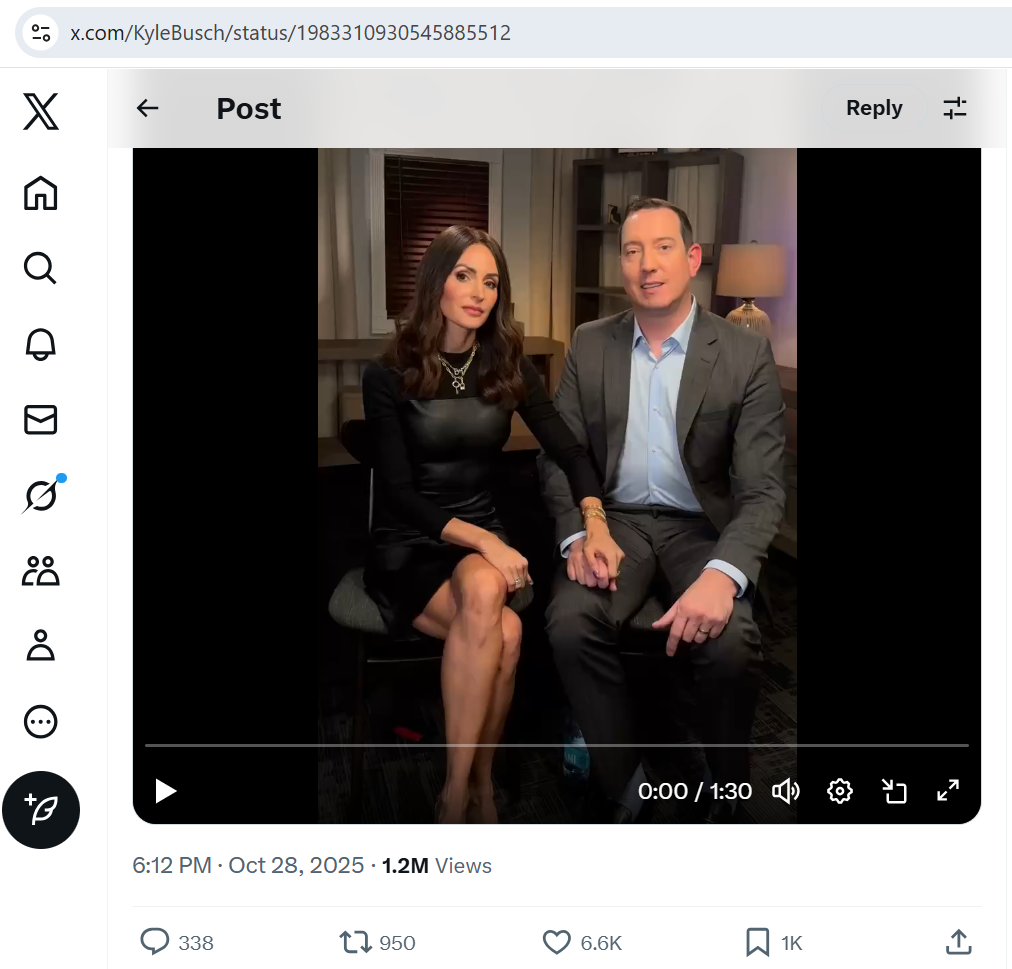

In a video with 1.2 million views that the Busches

“We’re out here speaking out about what happened, because this isn’t just happening to athletes and celebrities,” Samantha Busch said in the video. “This is happening to teachers, police officers, veterans —”

“Widows,” Kyle added.

“They’re widows,” Samantha Busch continued. “These are people who are 70 years old. They have nothing else to fall back on. These are people who have worked hard, they’ve made a small business. They are ready to retire, and they buy into these scams and they lose absolutely everything. So you know Kyle and I will use this platform to try to do all the good that we can and so we’re going to keep fighting Pacific Life and we’re going to show the world that this was a huge and utter scam.”

The lawsuit quickly drew notice across both sports and insurance worlds, with industry outlet InsuranceNewsNet asking if it

For advisors and their clients — as well as insurance agents, trustees of trusts with life insurance and other financial professionals — the allegations present a cautionary reminder to order “inforce illustrations” from carriers showing the current and projected policy value, Hood said.

“I would order inforce illustrations for the policies that I was aware of for every client,” he said. “The best protection here is transparency, documentation and ongoing review. … If I was an agent, I’d order inforce illustrations for all of my insurers from all the carriers in which I did business to protect themselves from carrier misrepresentations too, because that can easily happen. That can very, very easily happen here. So the bottom line is, you know what? We don’t know the other sides of the story. It may well be that either the agent or the carrier turn on each other. I expect some of that to happen at some point, but it may be that they simply turn the cannons back on the Busches. So you know, what due diligence did you do in your capacity as trustee to buy these policies, become the owner and beneficiary of the policies?”

READ MORE:

Allegations of negligent financial advice

The lawsuit accuses Pacific Life and Smith of negligence and negligent misrepresentation, violations of a North Carolina law against unfair and deceptive trade practices, and breaches of their fiduciary duty. The Busches lost more than $8.5 million after paying $10.4 million in premiums and commissions for Pacific Discovery Xelerator policies and a later 1035 exchange that “were engineered not to maximize value for the policyholders, but to maximize commissions for Pacific Life’s distribution network and its agent,” the complaint said.

“These policies were not just poorly structured, they were actively designed to fail under the weight of excessive fees and commissions,” it said. “This policy was designed in such a way that benefited Pacific Life and its agent at plaintiffs’ expense, ensuring that the policies would erode in value and ultimately fail once the commission revenue had been realized.”

The Busches argue that Smith and the insurer’s pitch of tax-free retirement income involved the work of a financial advisor providing wealth management and estate planning-related advice that extended beyond merely a sales transaction. Besides the sheer size of the commissions, the lawsuit attacks the products’ structure.

“Indexed universal life products, and particularly Pacific Life’s Pacific Discovery Xelerator (PDX and PDX2) policies, are among the most complex financial instruments marketed to consumers,” the complaint said. “These products combine life insurance, derivatives-based index crediting strategies and variable cost structures that even seasoned investors cannot readily decipher. The policies include multiple proprietary indices, participation rates, multipliers, caps, thresholds and riders such as the ‘enhanced performance factor,’ each of which affects performance in ways that cannot be predicted or understood without specialized actuarial and financial training.”

By paying $1 million annually for half a decade, the Busches expected to get withdrawals of up to $800,000 per year by the time Kyle Busch, 40, would turn 52,

“The Pacific Life Indexed Universal Life policies sold and implemented through Smith violated basic suitability and disclosure standards and failed to reveal the true risks associated with variable interest crediting, policy charges, underperformance and potential policy lapse,” the complaint said. “Smith and Pacific Life represented that the policies would be fully funded and self-sustaining after a limited number of annual premium payments, and would thereafter generate substantial, tax-free income for retirement. Those representations were negligent and false. The illustrations and sales materials emphasized hypothetical growth rates and multiplier effects that could not be sustained under real-world market conditions, and neither Smith nor Pacific Life disclosed the sensitivity of the policies to cap reductions, policy expenses or changes in non-guaranteed elements.”

READ MORE:

Upshot for financial advisors and other industry professionals

The fact that the Busches are public figures, combined with the underlying complexities of IUL policies, means the industry will be watching as Pacific Life and Smith respond to the allegations and the case proceeds in court, Hood said.

“It’s gotten more complicated by the fact that the Busches not only filed suit against the insurance carrier and the agent, but they made it a cause celebre,” Hood said. “Whatever ends up happening, what we now know, with some evidence, is itself rich with lessons on both how insurance companies as well as their agents should conduct themselves.”